Risk Models Behind World’s Best Hedge Fund Strategy Are Getting a Lot Harder to Crack

As the best hedge fund strategy of 2023 becomes a magnet for mainstream investors, the risk models it relies on are getting a lot tougher to crack.

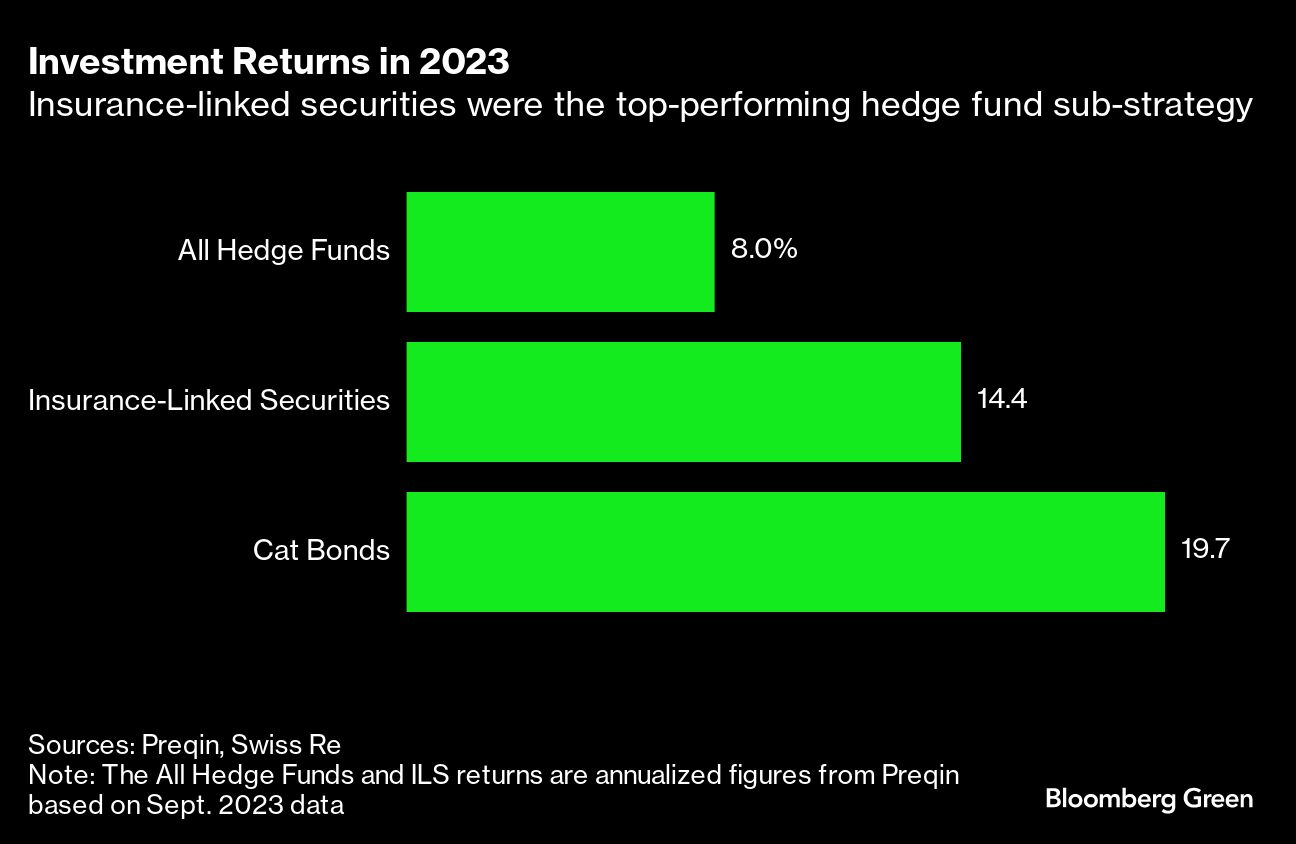

The strategy in question is tied to insurance-linked securities, which are dominated by catastrophe bonds (often dubbed cat bonds). In 2023, no other asset class produced a better-performing bet for hedge funds, with firms including Fermat Capital Management and Tenax Capital booking their biggest-ever returns.

Cat bonds have been around for more than 25 years and are used by the insurance industry to shield itself from losses too big to cover. That risk is instead transferred to investors who lose money if a pre-defined catastrophe hits, and rake in potentially huge returns if it doesn’t.

But calculating catastrophic risk is much more complex than it used to be. That’s because there’s a growing concentration of property in areas that are prone to increasingly frequent storms, fires and floods. Taken individually, each event is less intense than a major earthquake or hurricane. In aggregate, however, such losses can be a lot bigger, and that has major implications for the growing numbers of investors now adding exposure to cat bonds.

{kind=link}

Such secondary perils — mostly in the form of destructive thunderstorms — aren’t being consistently captured by models designed to measure cat bond risk, according to fund managers monitoring the development.

“We see that some models are actually not pricing these perils adequately,” said Etienne Schwartz, head of investment management at Twelve Capital, which holds $3.7 billion of cat bonds. In fact, he says “the expected loss on paper is way below what we actually think it is.”

Today, about 40% of cat bonds are for aggregate losses that accumulate over a single year, which is where investors are most likely to feel the fallout of secondary perils. The rest of the market is tied to losses that stem from one-off calamities such as a major hurricane, according to Artemis, which tracks the ILS market.

Globally, the total market for insurance-linked securities reached about $100 billion at the end of the third quarter, Aon estimates. Cat-bond issuance alone hit an all-time high of more than $16 billion in 2023, including non-property and private transactions, bringing the total market for the securities to $45 billion, according to Artemis.

After delivering returns of roughly 20% last year, cat bonds are now attracting many investors who would otherwise have avoided such a high-risk bet.

“Most of the clients that missed out on 2023, they now want to participate in 2024,” Schwartz said.

Investors who have been in the market a bit longer, meanwhile, are getting more discerning and moving away from bonds that are exposed to secondary perils, according to Andre Rzym, partner and portfolio manager at Man AHL, a unit of Man Group Plc, which is the world’s largest publicly traded hedge fund manager.

“Over the last few years, there’s been a drift in the market toward more per-occurrence deals,” namely those where the risk profile is tied to a single catastrophic event, Rzym said. And that’s “precisely because of this concern over secondary perils,” he said.

Elementum Advisors, which has invested about $2 billion in cat bonds, also is avoiding bonds that are exposed to mid-sized natural disasters.

“We don’t see a lot of benefit to our portfolios to add secondary perils,” said John DeCaro, co-founder and senior portfolio manager at Chicago-based Elementum. “There are a lot more variables and an element of randomness.”

Artemis estimates that the current 40% share for aggregate-loss bonds is down from more than 50% as recently as mid-2021.

Meanwhile, secondary perils are gaining in importance in climate science. A paper published by the University of Cambridge Institute for Sustainability Leadership noted that “rising secondary peril losses are the canaries in the coal mine when it comes to the disruptive economic impacts caused by climate change.”

Karen Clark, who has modeled natural catastrophes for more than three decades, says a good deal of her focus nowadays is on trying to perfect models for secondary perils such as floods, wildfires and severe convective storms.

“Climate change isn’t affecting the tail — the 1-in-100-year event — nearly as much as it’s increasing the 1-in-10-year, 1-in-20-year and 1-in-30-year losses,” Clark said.

At the same time, more infrastructure and homes sit in the path of mid-size disasters, adding to the potential for losses, according to Paul Schultz, chief executive officer of Aon Securities, a unit of Aon.

Secondary perils in the form of severe convective storms caused $133 billion of insured losses between 2018 and 2022, up 90% from the previous five-year period, according to Swiss Re. The insurer sought to draw attention to the danger as far back as 2019 in a paper titled, “Secondary Perils — Not So Secondary.”

Part of the challenge in modeling for such weather events is the lack of historical data. Unlike the models for a Florida hurricane or a California earthquake, which are built on a century and a half of data and increasingly sophisticated algorithms, loss estimates for a tornado or wildfire are less reliable.

The risk assessment also gets shaky when secondary perils, such as a wildfire, are bundled together with peak perils, like a hurricane. That’s because the extra uncertainty of a wildfire may not be captured in the cat bond’s loss probability.

“When there are cat bonds covering all natural perils with an expected loss inside 1% and a mid-double-digit issuance spread, alarm bells should start ringing,” according to a recent report from Marco della Giacoma, a portfolio manager at Tenax, and Toby Pughe, an analyst who also works at the London-based hedge fund.

The upshot is that it’s unclear what the shifting pattern of natural perils means for the cat bond market.

“There is a risk that secondary-peril loss trends might deter some new capital from entering the market,” Pughe and della Giacoma of Tenax wrote. And it also may “cause some existing investors to reassess their commitment to cat bonds,” they added.

- IBM, AT&T Accused by Whistleblower of Covering Up Foreign Hacks

- Insurance Attorneys Flip $1M Hail Claim into Nearly $2M Suit for Contractor Interference

- The Future of Appraisal and the Rising Standard of Competency

- Trump Will Ask Supreme Court to Revive $475 Million CNN Suit