Twice as Many Personal Lines Insurers Downgraded by AM Best in 2023

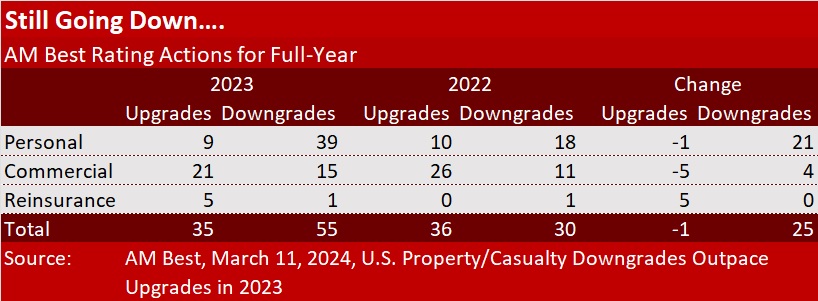

AM Best delivered 39 downward credit rating actions to U.S. personal lines insurers in 2023, more than twice the number registered for 2022, the rating agency reported in it official tally for the year.

Additional downgrades of 15 commercial insurers and one reinsurer brought the U.S. property/casualty insurance industry total to 55 for all of 2023 compared to 30 in total for 2022, the rating agency said in a report published yesterday.

{kind=link}

Although upgrades outnumbered downgrades for both commercial carriers and reinsurers in 2023, only 9 of 48 up-or-down rating actions for personal lines insurers actually brought their credit ratings up. The personal lines cohort saw downgrades soar to more than twice the number recorded in 2022 (to 39 from 18).

Auto carriers accounted for 24 of the personal lines downgrades, and all of the downgrades in the personal lines segment included a dimmer view of balance sheet strength, one of the “building blocks” that drive AM Best rating actions. The AM Best report notes that many of these downgrades were fueled by changes to multiple building blocks, which also include operating performance, business profile and enterprise risk management.

“Declines in capitalization and deteriorating operating performance drove the rating downgrades in the personal lines segment,” said Helen Andersen, industry analyst, AM Best, in a statement.

The few personal lines insurer credit rating upgrades, on the other hand, were largely not related to building block improvements. Instead, 60 percent were related to lift created by greater support from a parent organization or companies being integrated into higher-rated rating units.

For the three segments combined—personal, commercial and reinsurance—rating downgrades represented 7.4 percent of all AM Best rating actions in 2023, which also include initial ratings (25), affirmations (585) and actions to place ratings under review (41).

The under-review actions for 2023, mostly with negative implications, were almost double the number placed under review in 2022 (24), with the 2023 total representing 5.5 percent of all rating actions last year.

There were also seven fewer initial ratings assigned in 2023 than in 2022 (25 in 2023 vs. 32 in 2022). The bulk of last year’s newly assigned ratings, 19, were in the commercial lines segment. Five were in the personal lines segment and one was a reinsurer, AM Best said.

One of the commercial insurers with newly assigned ratings in 2023 is already under review. On Friday, AM Best announced that it had put the A-minus (Excellent) financial strength rating of members of Pie Insurance Group under review with negative implications, along with the long-term issuer creating rating of a-minus (Excellent). The rating agency said “material underwriting losses brought on by adverse reserve development in its New York book of business” prompted the action on the workers comp InsurTech.

“Although reserves have stabilized since third-quarter 2023, the magnitude of the development is concerning and has had an adverse impact on Pie’s risk-adjusted capital position,” AM Best added in a statement.

AM Best has also removed the “under-review” status from at least two property/casualty groups in recent weeks—affirming ratings for GuideOne Insurance Companies, a commercial casualty writer, and Stillwater Insurance Group, writing personal property.

Early last month, Best removed the “under-review” status from GuideOne’s A- financial strength rating and a- long-term issuer credit ratings, highlighting a strategic capital investment of $200 million made by Bain Capital Insurance, as a reason for the change. While balance sheet strength is strong, other building blocks are weaker—operating performance is marginal, business profile is neutral and enterprise risk management, appropriate.

“The [Bain] investment puts GuideOne in a much stronger capital position following significant surplus deterioration in 2022, driven by a net loss along with unrealized capital losses, as well as some deterioration through third quarter 2023 due to continued underwriting losses and other losses,” AM Best said.

AM Best’s GuideOne rating announcement also described the creation of The Mutual Group from Bain’s acquisition of GuideOne Insurance Company’s operational platform. The Mutual Group will act as a full-service insurance operations service provider for small to mid-sized mutual insurance operations, including GuideOne.

In removing the “under-review” status, AM Best assigned a negative outlook to GuideOne’s ratings, reflecting “the continued pressure on GuideOne’s balance sheet strength assessment.” While AM Best referenced the fact that “unprofitable underwriting performance related to the specialty business has negatively impacted its capital levels in recent years,” the rating agency also noted “significant actions the company has recently taken, including the exit of the specialty business” to improve underwriting results and the capital position.

AM Best similarly removed the “under-review” status while assigning a negative outlook to Stillwater’s affirmed financial strength (A-minus) and long-term issuer credit ratings (a-minus), assessing balance sheet strength as strong, operating performance as adequate, business profile as neutral and enterprise risk management, appropriate.

Among the issues that caused AM Best to place Stillwater’s ratings under review last year were “a significant decline in its surplus position at year-end 2022 from substantial unrealized capital and net underwriting losses,” with unfavorable underwriting results continuing in 2023. The unrealized capital losses were driven by the equity markets volatility, while underwriting losses related to “multiple fire losses and weather-related events, as well as rapid and atypical increases in inflation that have plagued the entire industry,” Best said, noting that Stillwater’s homeowners line of business accounts for about 72 percent of its premium volume.

“The removal of the under review with negative implications status is based on a series of initiatives implemented by management to replenish capital, [including] a capital infusion from its parent, the implementation of a quota share reinsurance treaty for the property book of business, increased top layer catastrophe coverage and a further reduction of common stock holdings in the investment portfolio to remove market risks.”

Looking ahead, Best stated, “The expectation is for operating metrics to improve in the near term to alleviate further pressure on capitalization. Further deterioration in operating results or overall risk-adjusted capitalization could potentially result in a downgrade in either the balance sheet or operating performance assessments.”

As for what’s in store for other rated entities this year, Anderson said, “AM Best expects market trends to continue to have a negative impact on the U.S. personal lines insurers.”

“Carriers that are slow to address challenges or do not have the means, expertise or technological capabilities to keep pace with changes in the environment will likely face ratings pressure,” she said.

- Citigroup Settles $70 Million Trade-Loss Suit With Loomis Sayles

- AI Skills More Valuable Than MBAs, 86% of Finance Executives Say

- Bodily Injury Is Now A Big Share of Auto Claims Payouts. Is AI to Blame for That Too?

- Humans, Not AI, Still A Cause of Most Cyber Losses in First Half of Year