Florida’s Home Insurance Industry May Be Worse Than Anyone Realizes

Seven property insurers in Florida went bankrupt in 2021 and 2022. The bankruptcies left thousands of homeowners scrambling to get new coverage, which often came with a big increase in cost. Worse, many had outstanding claims for hurricane damage that had not been addressed.

Jacqueline Ravelo, a Miami homeowner, was among them. Her roof was damaged by Hurricane Irma in 2017. Her insurance company, Avatar Property and Casualty, covered the cost of some repairs. But the roof continued to leak and mold grew inside the house, she said. Ravelo sued Avatar to compensate her for further repairs, which she said came to $50,000. When they were on the verge of settling, she said, the company went out of business.

Avatar and the six other companies that folded had something in common: They had all been rated A (“exceptional”) or higher by Demotech, Inc., an Ohio-based insurance ratings firm. (One of those insurers was also rated A- by competitor AM Best Co. Inc.)

In fact, nearly 20% of the companies doing business in Florida that Demotech rated as financially stable went insolvent during the period 2009 to 2022, according to a working paper by researchers at Harvard University, Columbia University and the Federal Reserve that was released by Harvard Business School in December. In their data sample, 99.7% of the ratings issued by Demotech were an A or above.

That’s a signal, the researchers said, that Florida’s insurance market may be full of weak players and is even more precarious than already known.

“Our research shows that lax regulation and monitoring of property insurers makes Florida mortgage markets far more exposed to climate risk than people might think,” said Parinitha Sastry, an author of the report and an assistant professor of finance at Columbia Business School. The paper has yet to be peer reviewed.

{kind=link}

The authors say this rating system also allows lenders making the riskiest mortgages to pass their liability on to everyone else.

US government-sponsored enterprises (GSEs) that secure mortgages — better known as Fannie Mae and Freddie Mac — demand that insurance meets a certain minimum quality standard. That’s especially important in places experiencing more severe catastrophes due to climate change, like Florida. When poor-quality insurance is graded as high-quality, it allows lenders in Florida to move mortgages for homes in vulnerable areas onto the books of Fannie and Freddie, who then bear the liability if they go south. Both GSEs will accept a rating from Demotech that is A or higher.

Demotech’s president and co-founder Joseph Petrelli disputed that his agency’s ratings are inflated in any way, calling the paper a “hit job.” He said he was “as surprised as anyone” when those seven firms declared insolvency, and that the real problem with the state insurance market is consumer and contractor fraud. Florida politicians have long blamed high insurance rates on excessive litigation: The state in recent years accounted for almost 80% of all US lawsuits related to property claims, due in part to a rule that let homeowners transfer insurance benefits to contractors.

Petrelli said litigation is escalating in a way his company couldn’t have anticipated. He cited evidence of law firms backed by deep-pocketed investors that use search engine optimization to find homeowners who want repairs done, and then encourage them to bring suit. “They were targeting insurers,” he said.

Jesse Keenan, a Tulane University associate professor who researches the intersection of real estate and climate change and who was not involved with the Harvard analysis, said the findings are troubling. “It is pretty clear that Demotech ratings are not up to par with where you would expect them to be,” Keenan said.

Freddie Mac and Fannie Mae both declined to comment on Demotech’s ratings. A spokesperson for Freddie Mac noted that the serious delinquency rate for US single-family homes in its portfolio stood at 0.54% in February 2024, the lowest in nearly 20 years. That suggests the numbers are not yet bearing out the theory that they are taking particularly risky mortgages from Florida or anywhere else.

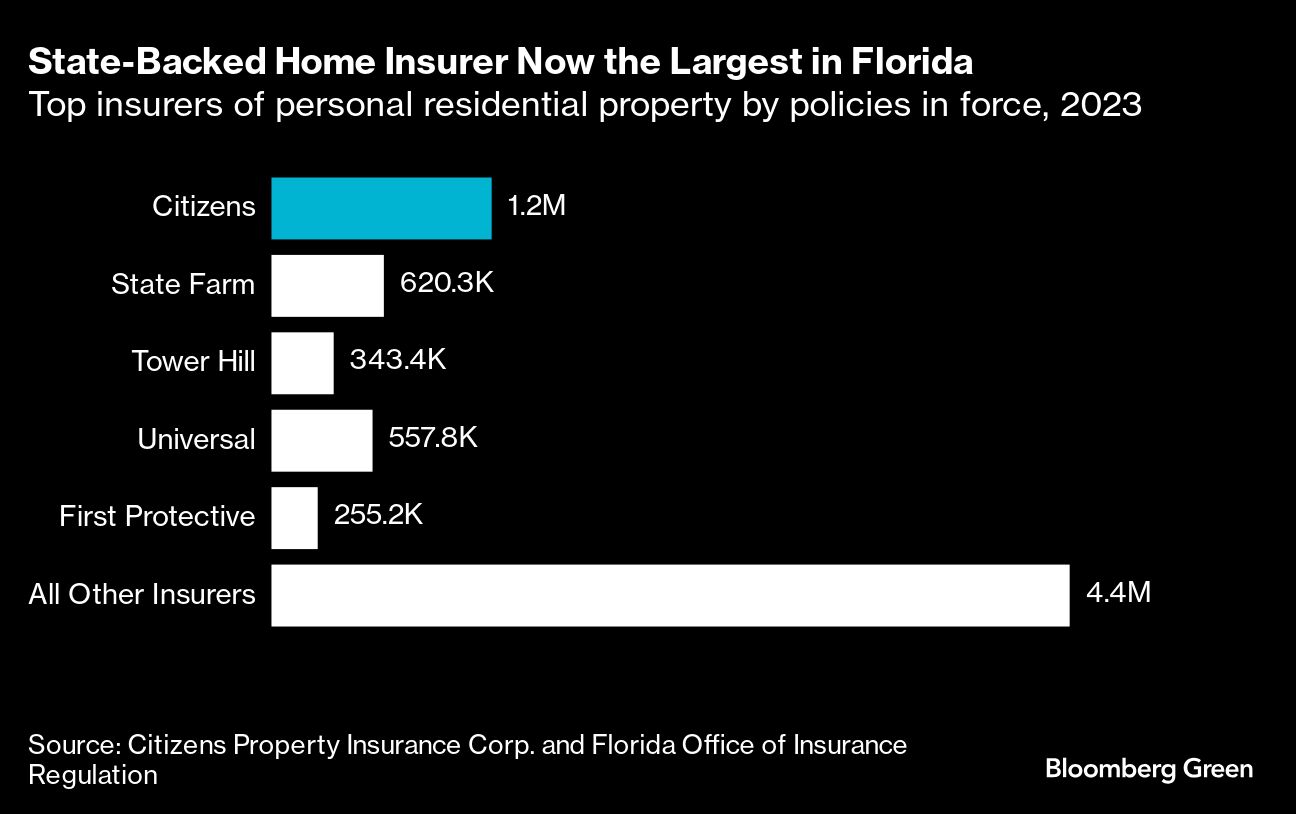

Florida, which has embarked on a building boom in some of the most hurricane-prone territory in the world, is contending with a well-publicized insurance crisis. Rates are now the most expensive in the nation, according to an analysis by Insurify. The state-backed insurer of last resort is now the biggest home insurer in the state and carries more than $500 billion in exposure.

The state’s struggle to hold onto private insurers is what brought Demotech to Florida in the first place. In the wake of 1992’s Hurricane Andrew, many Floridians were denied coverage by the private market. So they turned to the insurer of last resort, Citizens Property Insurance Corp. The state, for its part, tried to get people back onto private insurance. But many larger companies were shrinking their exposure to the riskiest markets.

{kind=link}

State-Backed Home Insurer Now the Largest in Florida | Top insurers of personal residential property by policies in force, 2023

That left a lot of smaller, less diversified insurers with less capital to take their place. It’s difficult for such insurers to get a top rating from AM Best or Moody’s Corp., whose methodologies mark companies down for those very qualities.

Demotech rates the smaller firms with a different methodology that it says is more appropriate to them. (Its website features a dragonfly and a T-Rex, noting it’s the smaller animal that has evaded extinction.) This approach allows insurers a higher reinsurance to capital ratio. Unlike capital reserves, reinsurance can be canceled. Since 1990, both Fannie Mae and Freddie Mac have deemed companies with an A or better rating from Demotech as acceptable.

Petrelli said that after Andrew, the then-commissioner of the Florida Office of Insurance (now the Florida Office of Insurance Regulation) begged Demotech to help the state, and in 1996 he agreed to. “We really stepped up” in a time of need, he said.

Michael Yaworsky, the current commissioner of the Florida Office of Insurance Regulation (FLOIR), said he couldn’t speak to the circumstances around Demotech entering the Florida market.

In a very short time, however, Demotech went from having no business in Florida to rating at its peak well over half of property insurers there. The company rated 95% of the insurers who accepted policies being transferred from the state-back insurer, Citizens, according to the Harvard paper, allowing Florida to depopulate its state program. In 2012, 200,000 state policies were transferred to Demotech-approved insurers, the Harvard paper added.

Using a database kept by the National Association of Insurance Commissioners, the researchers tracked insurance company liquidations in Florida between 2009 and 2022. They found that “19% of Demotech insurers entered rehabilitation proceedings in the past decade, while none of the traditional insurers did.”

Petrelli criticized the researchers’ methodology but said he wasn’t surprised at the figure: After all, Demotech dominated the market, so it makes sense that a disproportionate share of the bankrupt companies would be its clients.

Yaworsky said the Harvard study is based on “dated” information and rejected the idea that small insurers in Florida are weak. The main cause of insurance failure in the state in 2021 and 2022 was “pervasive and abusive insurance fraud,” he said. Legislative reforms passed in 2022 are already turning the insurance market around, he says: Eight new insurers have entered the state.

“Three insurers announced recently that they’re actually going to be filing with us to reduce their property insurance rates,” said Yaworsky. “This study cites data from over a decade ago. It seems to me that the market and the industry has moved on.”

There are fewer than a dozen companies registered with the U.S. Securities and Exchange Commission to provide credit ratings for insurance companies in the US. Some are familiar names, like S&P Global Inc. But Demotech is rare in specializing in rating smaller companies. Only a few such companies have ratings accepted by Fannie and Freddie.

Raters use different methodologies, and their grades don’t necessarily match up. The authors of the study ran a model to compare Demotech’s ratings to those of a larger competitor, AM Best. The researchers independently devised a facsimile of AM Best’s model and then used it to rate nearly 50 Florida companies that Demotech had in fact rated.

The exercise, they wrote, “suggests that the vast majority of these insurers would likely be rated ‘junk’ if they received their rating from a traditional rating agency rather than Demotech.” Or in other words, if Demotech were to use AM Best’s methodology, nearly two-thirds of its rated insurers would not meet Freddie Mac’s standards and 21% would not meet Fannie Mae’s.

Petrelli said this is conjecture. He noted the authors themselves admit their “counterfactual” model only explains close to 60% of the variation between Demotech’s and AM Best’s ratings. He said his own analysis of public filings shows that Demotech companies rated A or higher have similar rates of trouble over a 10-year period as AM Best companies rated B+ or higher.

Ishita Sen, a co-author and an assistant professor of finance at Harvard Business School, told Bloomberg Green that the GSEs could be powerful watchdogs on insurance raters if they updated their criteria, which they set “at some point way back in the 1990s, and over time have not evaluated whether these thresholds mean the same thing,” she said.

Freddie Mac said it “regularly reviews insurance rating requirements to make sure they align with our overall risk appetite.” Fannie Mae said it periodically reviews rating requirements.

Petrelli said Demotech was accepted by Fannie and Freddie after extensive audits in 1989 and 1990. He said he assumes they must review that decision, but couldn’t recall either asking him for additional information.

Officially, it is not FLOIR’s job to monitor insurance raters, but that does not mean that they and other Florida officials aren’t watching closely. In fact, they’ve shown themselves to care passionately on the subject — just not in the way that might be expected.

In 2022, as insurance bankruptcies were mounting, a number of companies received letters from Demotech informing them their ratings could drop, state officials said and news outlets reported at the time. Florida politicians, instead of applauding Demotech for caution, went on the attack. Yaworsky’s predecessor at FLOIR, David Altmaier, accused the rater of wielding “inconsistent, monopolistic power.”

Florida’s Chief Financial Officer Jimmy Patronis wrote letters to Fannie and Freddie describing Demotech as a “rogue ratings agency” with a “dubious” methodology. He warned that if the lower ratings came to pass, it would cause financial chaos for millions of Floridians.

In the end, Demotech downgraded only four of those insurers. But the message was clear: Downgrades are a political third rail.

Patronis’s office even commissioned a study to find alternatives to Demotech, which encouraged insurers to use multiple raters. Yaworsky said much of Florida’s insurance market is now rated by more than one firm.

Meanwhile, financial chaos has already come to some people who held A-rated insurance.

After Avatar went under, Ravelo, the Miami homeowner, had to start her claims process all over with the Florida agency that guarantees insurance in case of failure. Almost seven years on from the original damage to her house, she has voluminous files but still awaits a payout.

If her mortgage didn’t require her to hold home insurance, she would now choose to go without it, she said: “I am paying $5,000 a year for insurance, but I’d rather pay nothing at all. I’ve lost faith in the system.”

Top photo: Single-family houses in Palm Beach, Florida, U.S., on Wednesday, April 7, 2021. Purchase contracts for single-family houses priced at $10 million or more surged 306% in March from a year earlier, the biggest gain since the pandemic started, appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate said in a report.