The US’s Flood Insurance Program Is Making More Repeat Payouts

When Hurricane Helene barreled ashore last week, it caused devastating flooding across the southeastern U.S., including in the Shore Acres area of St. Petersburg, Florida. The neighborhood saw 6 feet of storm surge, which flooded roads and homes.

It was far from the first time.

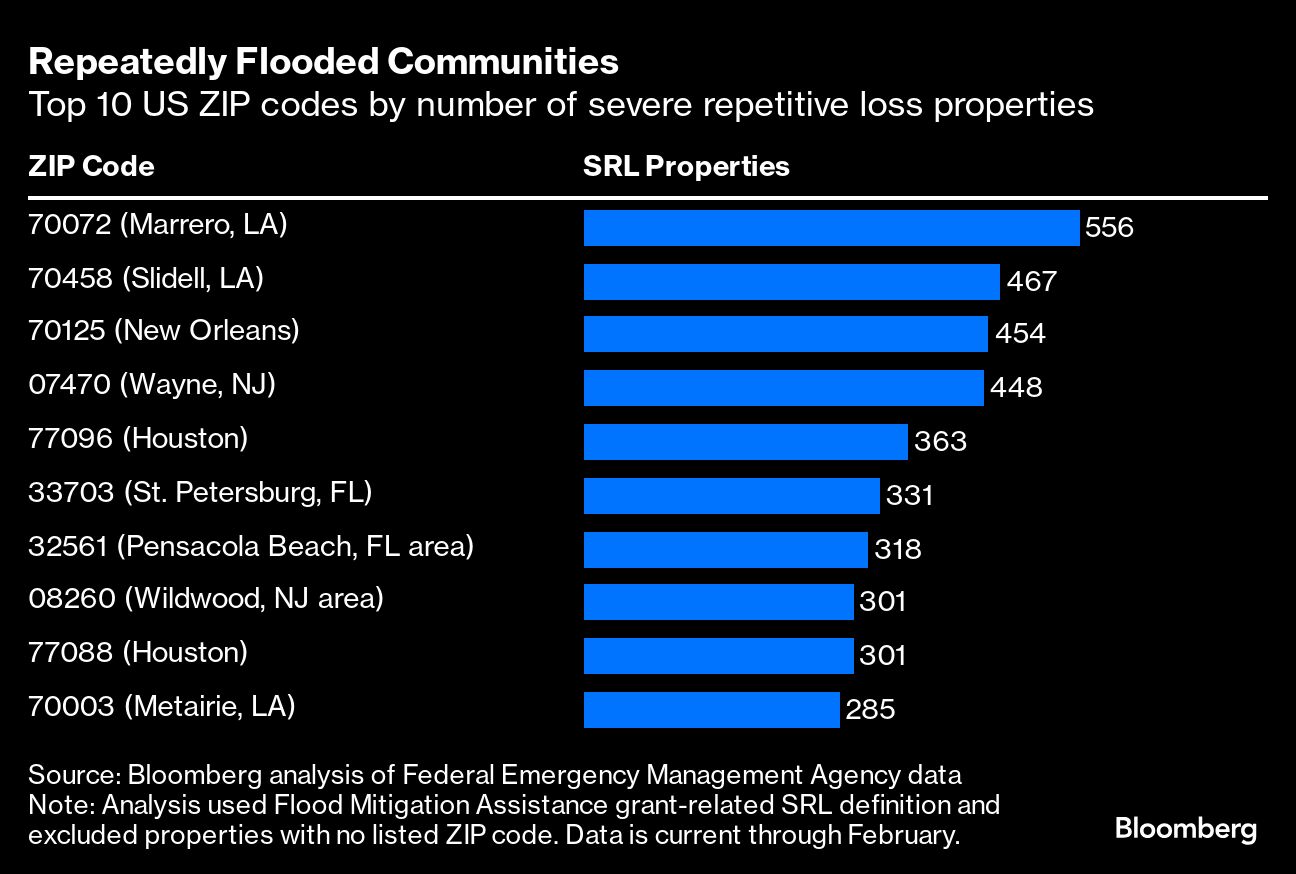

Shore Acres, where roads are just 2 feet above sea level at their highest point, sits in one of the 10 ZIP codes with the greatest number of “severe repetitive loss properties.” It’s a designation used by the Federal Emergency Management Agency (FEMA) and the Natural Resources Defense Council (NRDC) to refer to primarily residential buildings that have received at least four flood insurance payouts totaling $20,000 or more, or at least two totaling more than the building’s market value.

Related: Modeler KCC Puts Privately Insured Losses at $6.4B From Helene

Severe repetitive loss (SRL) properties are a growing category. NRDC identified about 40,000 of them in 2022, in an estimate that associated the majority of SRL properties with their rough dates of designation. That was up from about 10,000 SRL properties in 2000, a sharp increase that highlights the burden extreme rainfall and flood risk is placing on homeowners, landlords and insurers.

{kind=link}

“It’s a huge problem. It’s getting worse,” says Anna Weber, senior policy analyst for flooding solutions at NRDC. Because the data only covers properties that have had flood insurance coverage in the first place, it’s “just the tip of the iceberg,” she says.

Related: Hurricane Helene Halts Poultry Plants, Damages Cotton Crops

Only about 4% of Americans have flood insurance, though one analysis pegged that figure at 2.5% or lower for many of the inland counties affected by Helene. Roughly 95% of US flood insurance policies are issued by the National Flood Insurance Program (NFIP).

Using a slightly different methodology, FEMA counted about 46,000 buildings as SRL properties as of February, 8% of them in the top 10 ZIP codes. Eight of those ZIP codes are in Gulf Coast communities, where hurricanes are common. But it doesn’t take particularly extreme weather to spur flooding. Rainstorms cause flash floods in coastal Louisiana. New Jersey’s Wildwood is vulnerable to storm surges. Shore Acres is so low-lying that it can flood when it’s sunny.

Created in 1968, the NFIP plays a critical role in insuring homeowners for flood risk. But the program is also designed to incentivize people and communities to reduce that risk. Local governments that join the NFIP are required to adopt floodplain management regulations.

{kind=link}

“It’s generally accepted that climate is getting worse [and] flooding is getting to be more of a problem,” says Mark Browne, chair of the faculty for the School of Risk Management at St. John’s University. Browne says curbing flood risk is “increasingly important.”

Some communities are doing just that. New Jersey recently agreed to an emergency sand-pumping project to shield North Wildwood from storm surges, while St. Petersburg has upgraded valves that prevent bay water from flooding Shore Acres.

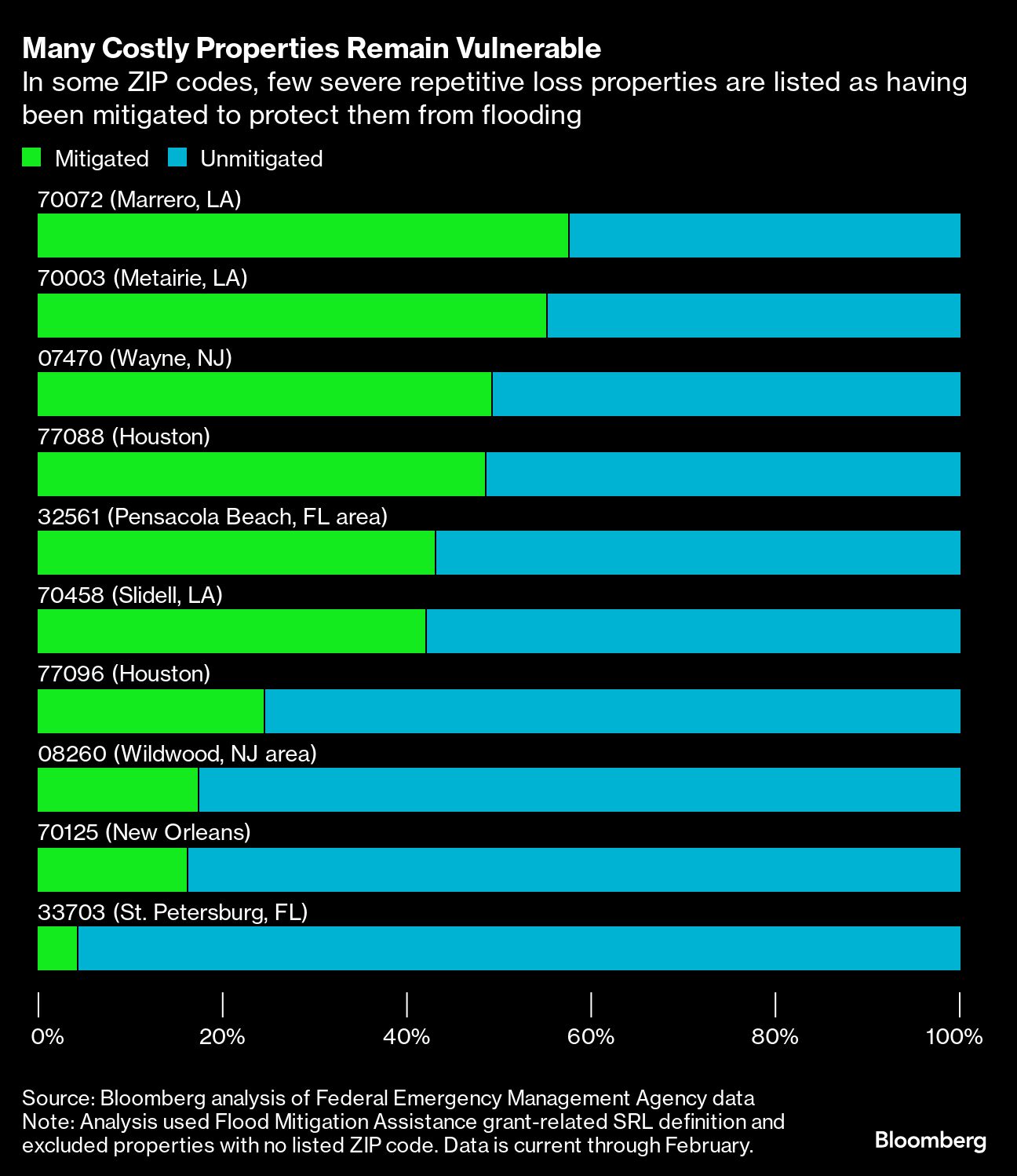

Still, many properties remain unprotected. In the Shore Acres-area 33703 ZIP code, for example, only 14 of 331 SRL properties are listed as mitigated — a designation that means a property has been fortified against flood damage.

Overall, protective steps have been taken for a little over a third of SRL properties in the top 10 ZIP codes, according to FEMA data. Nationwide, about 24% of SRL properties are currently mitigated, though Weber cautions that FEMA may have data gaps that cause it to understate the number of mitigated properties.

{kind=link}

While federal grants pay for projects that curb the risk of repeat damage to NFIP-insured buildings, there isn’t enough money available to meet every request, said Sandra Knight, a former FEMA official who oversaw mitigation grants and floodplain management. To stop repeat flooding, governments could also update zoning laws to prevent development in at-risk areas, she said, including by accounting for the way risk is changing along with the climate.

“Existing infrastructure that’s already there, that’s harder to deal with, because then you are going to have to mitigate or move,” Knight said. “And people don’t want to do that.”

Methodology: FEMA data defines severe repetitive loss properties in two different ways, both based on NFIP payouts. This analysis used a definition related to Flood Mitigation Assistance grants that does not reset if a property is mitigated. Properties with no listed ZIP code were excluded. The dataset was last updated in February.

Top photo: A search and rescue team member inspects a building in the aftermath of Hurricane Helene in Bat Cave, North Carolina, on Oct. 1.