Allstate Thinking Outside the Cubicle With Flexible Workspaces

After ditching two-thirds of its office space and selling its Chicago headquarters, Allstate Corp. realized that even employees who prefer working remotely still need a place to gather with their coworkers from time to time.

In the coming months, a quarter of the insurance giant’s 54,000 corporate employees in cities like Atlanta, Tampa and Minneapolis will be able to meet up with colleagues in offices booked by the day through a coworking platform called LiquidSpace. Others will work in traditional leased space where desks have been jettisoned for cozy cafes, quiet libraries and event spaces.

While companies like Amazon.com Inc., Goldman Sachs Group Inc. and United Parcel Service Inc., force staffers back to the office, and others remain fully remote, Allstate is trying to thread the needle with a mix of options that keep flexibility a priority but avoid asking workers to trudge into an office only to spend most of the day in front of their screens in virtual meetings.

“We’re building something new,” said Lauren DeYoung, who, as Allstate’s “workplace futurist,” is spearheading the transition. “When I talk to our people, they’re just so surprised we’re doing this, and trying something different.”

Allstate says there’s no going back to pre-pandemic days of vast offices around the U.S. The company slashed annual spending on corporate offices from $382 million in 2020 to $138 million this year, excluding the 7,100 local storefronts that individual agents own and operate.

Reason to Gather

Most of the ten Allstate employees who shuffled into a downtown Minneapolis conference room on a recent visit had never met before. When they entered, a whiteboard mistakenly welcomed employees of rival insurer Transamerica, not Allstate.

But employees quickly picked up on some of the value of being in person with their coworkers: “I get stale working in my apartment,” said Brittany Murphy, who usually works remotely on the company’s social-media team.

They had gathered inside Coco, a coworking site located in the city’s historic grain exchange building, to hear from Allstate Chief Executive Officer Tom Wilson about the importance of connections.

“I hope we can start to get to know each other, identify opportunities for collaboration and have some of that office chat,” said Sarah Springer, who usually works remotely in the company’s data analytics department. “But it’s early on.”

{kind=link}

While the employees communing over bagels that morning said they appreciated Allstate’s remote-first policy, which began during the pandemic, they had come to realize some shortcomings, like the lack of office mates to gossip and trade ideas.

Before the end of the day at Coco, Springer and other colleagues began coordinating follow up visits. Others planned a charity 5K run together, and there was talk of a happy hour later that evening.

“You want me to commute to an office? We’re open to that, as long as there’s a reason,” Springer said. “If you want me to come in and sit on Zoom all day, there’s no point to that.”

Fewer Cubicles

Allstate’s shift to coworking reflects its acknowledgement that the pandemic changed white-collar work irrevocably — and the insurance industry is no different.

Customers are now comfortable buying and managing policies online, while tasks like generating quotes and assessing car-accident claims can now be done digitally in minutes, rather than taking hours in person. “It used to be you got in a car accident, we drove out to your house, or we met you at a body shop,” Wilson said at a recent investor conference. “Today, you send us six pictures, and we do it in minutes. Adjusters can do over 20 [claims] a day, and pretty soon, the computer will do a bunch of them.”

That digital transformation requires far fewer cubicles.

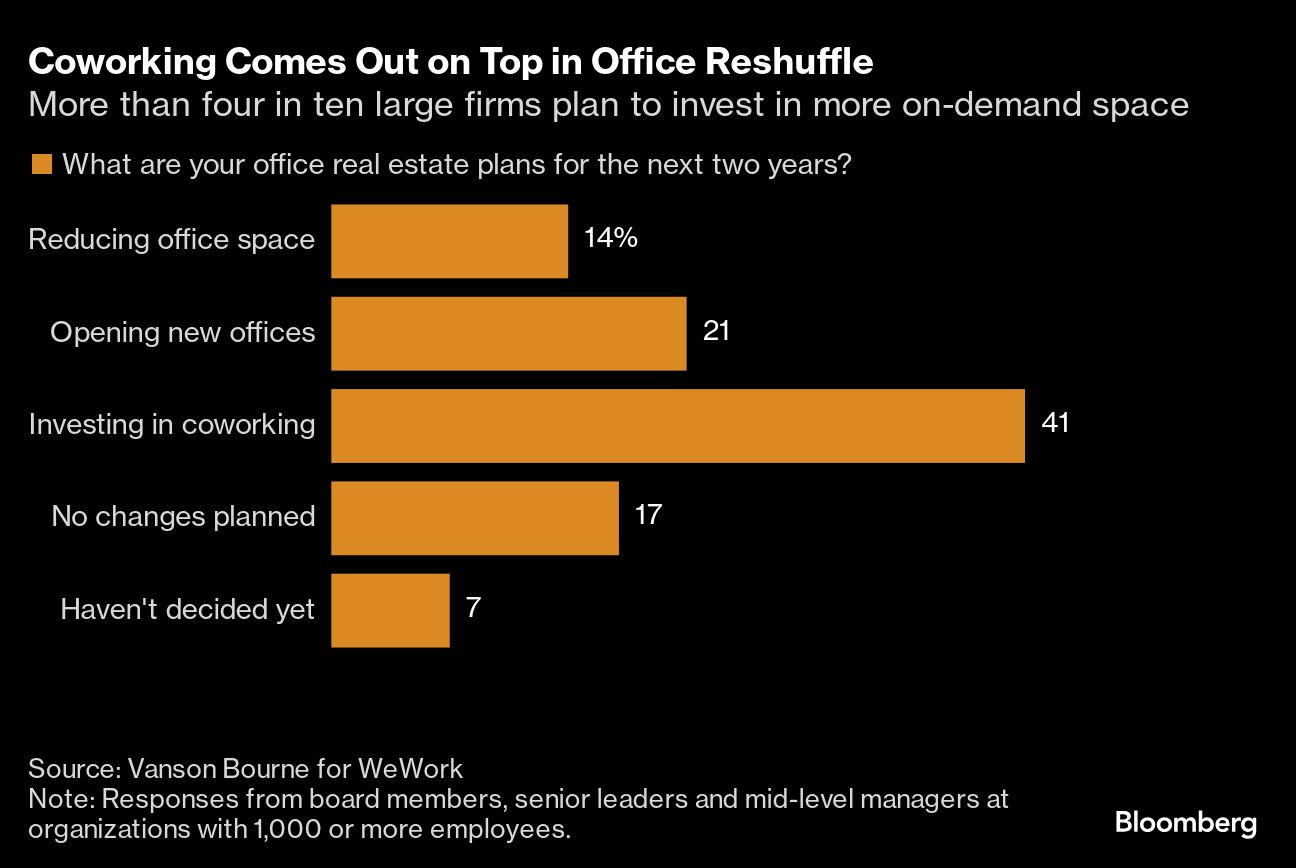

With hybrid-work now the norm at most white-collar organizations and office occupancy rates still stuck at around half of pre-pandemic levels in major US cities, firms have scrambled to jettison unneeded space.

Businesses now occupy 210 million fewer square feet than they did in April 2020, according to CoStar Group Inc., a commercial real-estate firm, and as of last year nearly two-thirds of them planned to make further reductions, according to Cushman & Wakefield. By contrast, there are now 7,538 coworking sites in the US as of October, up 22% over the past year, according to CoworkingCafe, a flex-space website.

“Workspaces need to be different than what they were,” Allstate’s DeYoung said. “The days of cubicle farms are over.”

As DeYoung tried to figure out what work needed to be done where, she discovered that employees needed more room for collaboration, but also quiet places to focus.

For example, Allstate’s office in Charlotte, North Carolina, now features a hushed, soundproof library where staff can study for their licensing exams, as well as nooks to grab snacks, and open space for bigger meetings.

On one floor, Jason Griffin, a senior manager in the complex-liability determination unit, shows new employees how to assess fault in collision claims. These newbies used to start off remotely, but so many struggled and quit that Griffin now requires them to be mostly in the office for the first few months. The in-person training helped slash voluntary turnover in Griffin’s department to 5% from about 35%.

“The self-starter can work from home,” Griffin said. “But another person might need to be nudged along a little bit.”

In places like Atlanta, Indianapolis, Minneapolis and Columbus, Ohio, Allstate has between 100 and 1,000 employees — too few to justify an office lease, but enough that there’s a need to come together once in a while for training, mentoring and team-building activities.

So DeYoung turned to Mark Gilbreath, founder and CEO of LiquidSpace, which offers more than 13,000 offices and meeting spaces globally.

LiquidSpace also counts big companies like wireless provider T-Mobile US as clients, which book daily locations in cities like Los Angeles where it’s shuttered offices, significantly reducing real estate costs in those areas. Amazon — which just told corporate staff they must soon be in the office five days a week — is also a big user of on-demand space in some markets. Gilbreath sees on-demand space being part of the mix of all big companies one day.

“It’s not just a real-estate play,” Gilbreath said. “They want to make this work.”

Allstate has reduced its footprint from 12 million square feet to 4 million, but it still needs space in certain places at certain times. “In some cities, we have people who do not have an easy way to know that other [colleagues] are even working in the area,” DeYoung said. In those regions, “we know that a five-year lease is not the right cost decision.”

A coworking membership for 10 employees — the size of Allstate’s September gathering in Minneapolis — is more affordable than an equivalent office lease in 97% of 102 US cities, according to CoworkingCafe.

Colorful History

Allstate’s alliance with LiquidSpace represents a bet on a working style that’s had its ups and downs in the US since a few Bay Area startup staffers rented space in a San Francisco feminist collective in 2005 and called the newfangled arrangement “Coworking.”

The fledging community grew and soon many laptop-toting creative types wanted to join the group, which relocated to larger digs the following year and eventually took up the new-age name “Citizen Space.”

“Coworking existed long before WeWork was even an inkling of an idea,” Tara Hunt, Citizen Space’s co-founder, said.

Similar communities soon sprouted in other cities. At the time, owners and managers of office real estate saw coworking as more of an oddity than an opportunity. Alex Hillman, founder of Indy Hall, a coworking group in Philadelphia, recalls the reaction when he explained to his first landlord that he’d be offering use of his 1,200 square-foot, split-level Old City loft to people who didn’t work for the same company but wanted to work from the same place: “They thought we were insane.”

When the 2008 financial crisis cratered real estate values, making space cheaper, coworking flourished. It allowed professionals and entrepreneurs to gather, swap ideas and socialize, with none of the politics and posturing of a traditional corporate office. “It was a path out of the old way of doing work that didn’t work for a lot of people,” said Tony Bacigalupo, who co-founded Manhattan’s first coworking space in 2008.

Adam Neumann set up WeWork’s first Manhattan locations in 2010 and over the next decade, gobbled up space as fast as SoftBank Ventures and other deep-pocketed backers could write checks. The coworking sector grew by an average of 22% each year, according to JLL.

WeWork’s fall from grace dented the reputation of coworking just as Covid hit, emptying offices across the US.

But as companies crept back , they found landlords happy to cut all sorts of deals to entice them. Sometimes, those deals include free use of communal spaces shared by all tenants — coffee bars, fitness studios, conference rooms and auditoriums.

“Today, it’s almost impossible for a landlord to provide a large office building without some flexible offering,” said Despina Katsikakis, the global lead of Cushman & Wakefield’s Total Workplace consulting and research business. Coworking sites also have blossomed in small towns and suburbs as employers see the payback of reducing the financial and psychic drain of commuting.

But coworking isn’t without challenges: While booking space is easy, it’s not always clear to employees who’s showing up where and when. And given that these spaces are on demand, pricing is “a little all over the place,” said Mike Thomas, Allstate’s vice president of administration and real estate. A few Allstate employees also grumbled that the wi-fi can be clunky in certain locations.

“We’re still testing and learning,” Thomas said. “What if we’re wrong? We will figure it out. For years the saying used to be, ‘Build it and they will come.’ Now, it’s ‘Let’s see where they go, and we will build there.'”

Top photo: Allstate colleagues Tim Venne, middle, and Hilary Fox, right, talk about their jobs at the coworking space Coco in Minneapolis, Minn., on Thursday, October 10, 2024. (Photo by Tim Gruber for Bloomberg).