The Evolution of Homeowners Insurance in California—From Niche to Necessity

For many years, the homeowners insurance market operated as a relatively stable and predictable sector in California. Changes were incremental, and the market largely catered to established patterns of risk and pricing.

This stability, however, has been disrupted recently, with dramatic shifts reshaping the landscape. The surplus lines insurance market has seen unprecedented activity, and 2024 marks yet another pivotal year in its evolution.

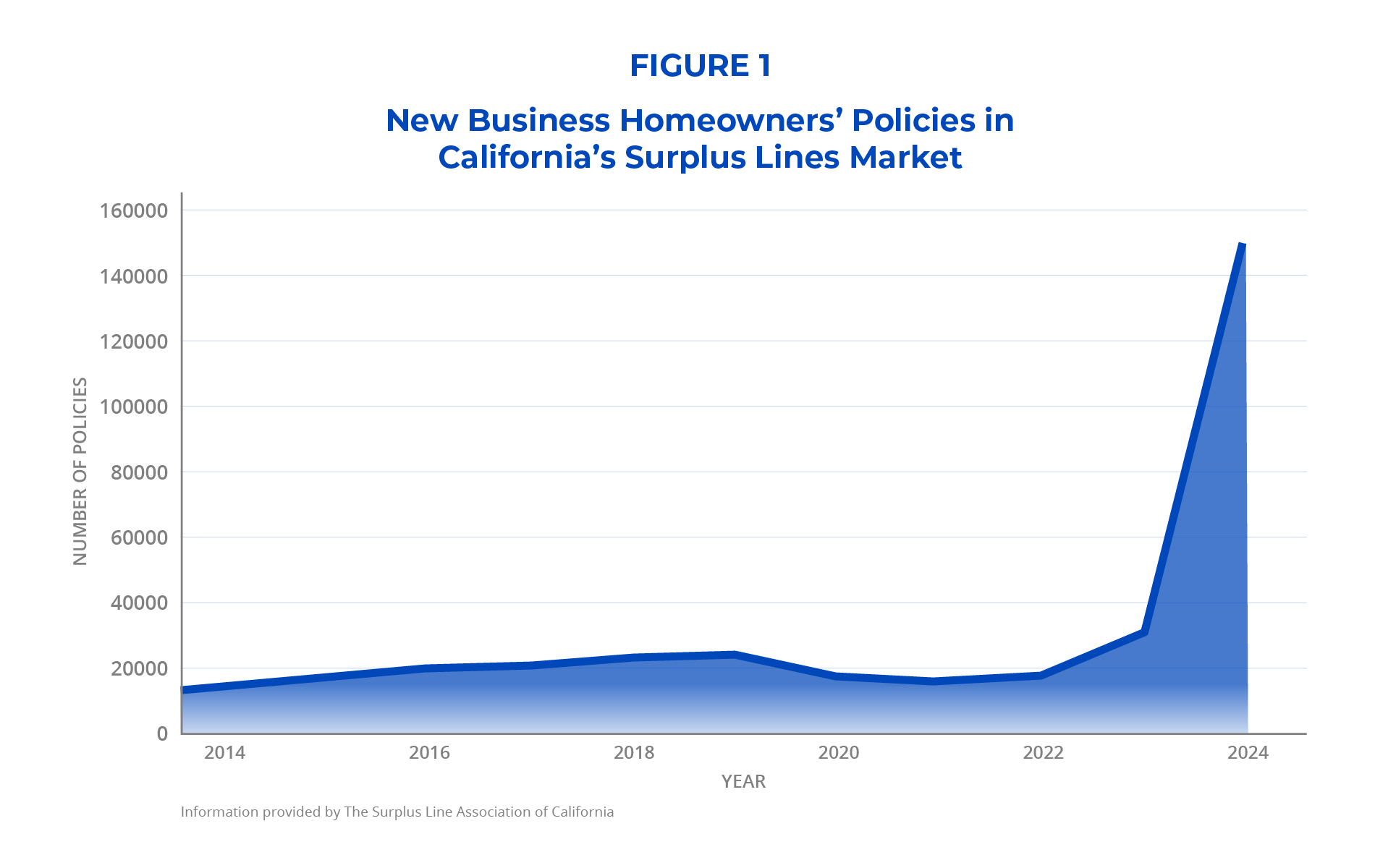

Building on the trends observed in 2023, the surplus lines market in California experienced remarkable growth in new business in 2024. The annual number of new business policies increased dramatically, from about 31,000 in 2023 to more than 150,000 in 2024—a staggering growth of 383% (Figure 1).

This sharp rise underscores the continued ability of surplus lines carriers to meet the increasing demand for homeowners insurance coverage left unaddressed by admitted carriers.

This growth reflects an expansion in the types of properties currently being insured in the surplus lines market due to admitted carrier withdrawals. Unlike admitted insurers, which are strictly regulated and subject to rate approvals, surplus lines insurers operate with more pricing flexibility, allowing them to insure risks that traditional insurers decline to cover.

Historically, surplus lines homeowners insurance policies have been associated with high-value, unique or high-risk properties, resulting in larger insurance premiums, higher replacement costs and more complex underwriting requirements. However, the data for 2024 paints a different picture, one that aligns more closely with the characteristics of policies typically associated with the admitted homeowners insurance market.

{kind=link}

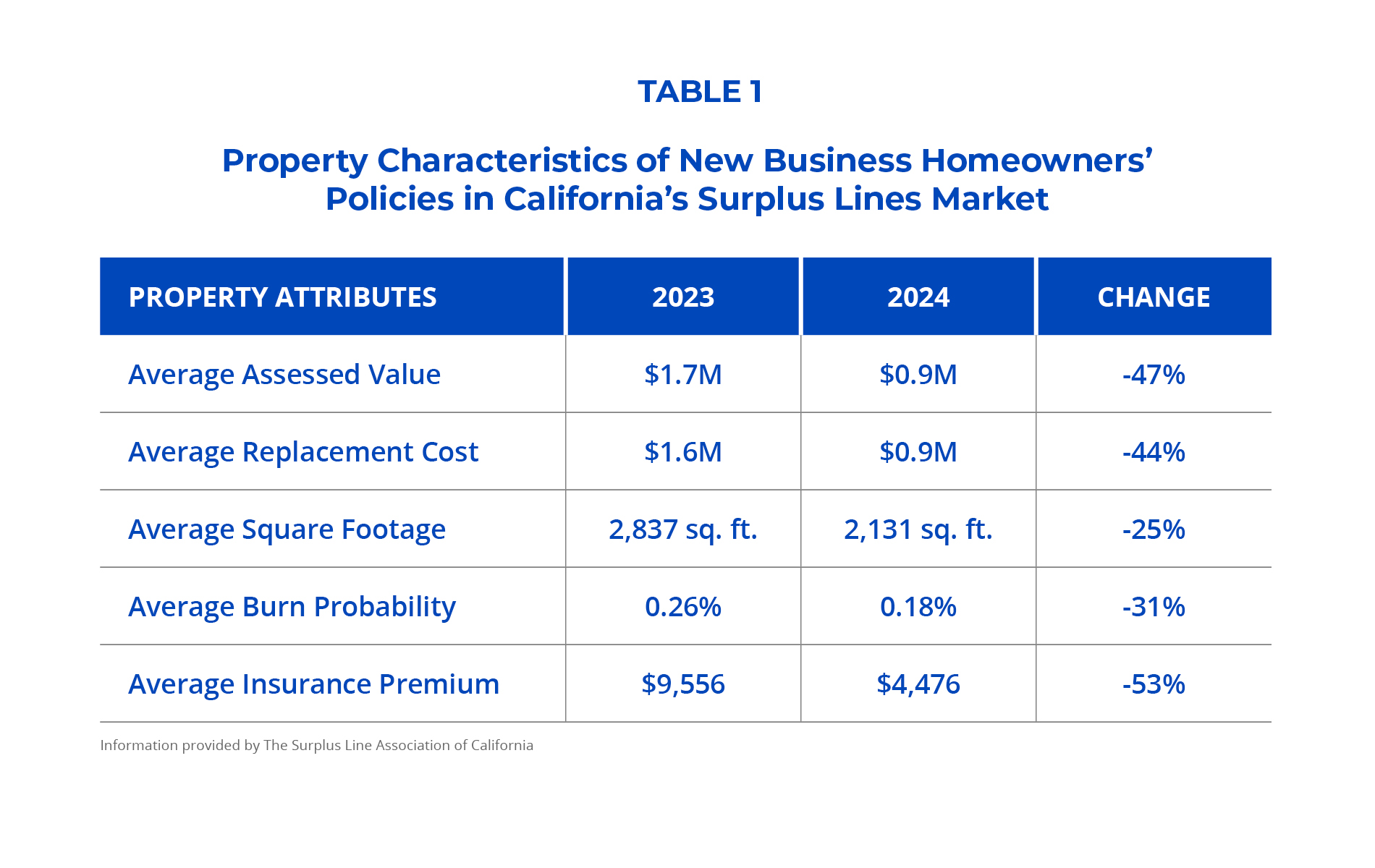

Data collected using e2Value and the U.S. Department of Agriculture highlights significant changes in key property characteristics for new business policies in California’s surplus lines market.

Assessed values for new business policies in 2024 averaged $0.9 million, a significant decrease of 47% compared to $1.7 million in 2023. Replacement costs experienced a similar decline, dropping by 44%, from $1.6 million in 2023 to $0.9 million in 2024 (Table 1). These reductions are substantial, indicating that the surplus lines market is increasingly insuring properties of lower value—properties that are less complex and were once comfortably within the scope of admitted carriers.

The shift is also evident in the size of properties. The average square footage of newly insured properties fell from 2,837 square feet in 2023 to 2,131 square feet in 2024, marking a 25% reduction. Additionally, the average burn probability—a metric indicating the annual likelihood of a wildfire occurring at a specific location—has decreased by 31%, from 0.26% in 2023 to 0.18% in 2024 (see Table 1). This decline suggests that the properties now entering the surplus lines market are in areas with lower wildfire risk, reinforcing the notion that these policies would have previously been placed with admitted carriers.

{kind=link}

At the same time, insurance premiums followed a similar trajectory, with the average premium for new business policies decreasing by 53%, from $9,556 in 2023 to $4,476 in 2024 (Table 1). These declining insurance premiums reflect not only lower-value properties but also shifting risk profiles that more closely align with the admitted market’s traditional scope. The convergence of smaller property sizes, reduced burn probability and lower premiums further supports the hypothesis that this growth is being driven by policies displaced from the admitted market.

The withdrawal of major admitted insurers, including Allstate and State Farm, has created significant coverage gaps, pushing homeowners toward the surplus lines market as an alternative. The properties now entering the surplus lines market reflect this shift, with significantly lower sizes, assessed values, replacement costs, wildfire risks and insurance premiums—demonstrating the extent of admitted carrier withdrawals and the market’s need for alternative solutions.

At the same time, the influx of traditionally admitted market–type properties changes the risk profiles of the surplus lines market, requiring insurers to adapt their underwriting and pricing strategies to accommodate this new reality. The continued growth and evolution of the surplus lines market in 2024 serves as a response to immediate market pressures, but long-term stability depends on restoring balance within the overall insurance system.

Gorshunov is a data scientist for The Surplus Line Association of California.

Top photo: The Palisades Fire in Los Angelas, January 2025. Source: CalFire.